Clearer cross-border money movement.

Globridge is building a consumer-friendly cross-border money account for people who support family, pay trusted recipients, and manage value across countries. See clear quotes, track transfer status, and use a product designed to keep backend complexity out of the user experience.

Globridge is in development. Public availability, features, limits, and payout options will depend on partner support, eligibility, legal review, and supported jurisdictions.

Illustrative quote only. Globridge fee shown before confirmation.

Example shown for illustrative purposes only. Final recipient amount, fee, exchange rate, delivery method, timing, and availability may vary at the time of transfer.

Built for cross-border money that people rely on.

Globridge is designed for recurring cross-border needs: supporting family, paying trusted recipients, and managing value across countries with clearer visibility and fewer moving parts.

Less fragmentation

Many users rely on separate apps for remittance, bank access, savings, payout status, and exchange-rate checks. Globridge is being built as a simpler cross-border money account.

Built around trust

For users sending money abroad, reliability matters as much as price. Globridge emphasizes clear quotes, visible transfer status, supported payout options, and support-ready records.

Backend complexity stays hidden

Customers should not need to understand payment routing, stablecoins, chains, wallets, gas fees, or settlement mechanics. Globridge handles supported infrastructure workflows behind the scenes.

Built for recurring cross-border support.

Globridge is designed for people who regularly support family, trusted recipients, and cross-border obligations. We are beginning with a controlled U.S.–Philippines launch before expanding availability.

What you should see before sending

Before confirming a transfer, Globridge is designed to show key details in one place so users can understand the transaction before they proceed.

Final recipient amount, fees, rate, delivery method, and timing may vary by corridor, eligibility, partner support, and transfer conditions.

How Globridge works.

A simple transfer experience backed by disciplined payment operations and partner-supported infrastructure.

Enter the amount

Review the estimated recipient amount, fee information, and available delivery method before sending.

Add a recipient

Create a recipient profile and select a supported payout option for the corridor.

Track the transfer

Follow status updates from funding to payout confirmation, with support workflows for exceptions.

Build account utility

Future account features may help recipients use funds more directly after arrival, subject to eligibility, partner support, and legal review.

Features designed around confidence.

Cross-border payments are not only about price. Users need clarity, reliability, recipient access, and support when something needs attention.

Clear all-in quote

Show the sender what they are paying and what the recipient is expected to receive before the transfer is initiated.

Transfer tracking

Status visibility helps users understand whether a transfer is pending, under review, processing, delivered, or requires support.

Repeat recipient flows

Built for recurring sender-recipient relationships rather than one-off payment activity.

Supported payout options

Payout availability will depend on corridor, partner coverage, eligibility, and local payment methods.

Simple user experience

Users should not need to manage chains, private keys, token tickers, gas fees, or self-custody workflows.

Customer support readiness

Operational workflows are being designed for transfer exceptions, refund handling, and customer communications.

Product roadmap.

Globridge is starting with cross-border transfer utility and will expand only after customer demand, partner readiness, compliance review, and operating controls are validated.

Launch product

Initial functionality is focused on a clear transfer flow: onboarding, recipient setup, quote review, funding, status tracking, payout confirmation, history, and support.

For senders

A more transparent way to support people across borders, with visible transaction status and a recurring-recipient experience.

For recipients

A planned account relationship that can grow beyond payout into balance utility and direct payments where supported.

Behind the scenes

Globridge may use approved payment and settlement infrastructure, including stablecoin-based workflows where appropriate, without making crypto the consumer experience.

Availability-controlled launch

Transfer size, destination coverage, payout options, and feature access may be limited during launch and expanded in stages.

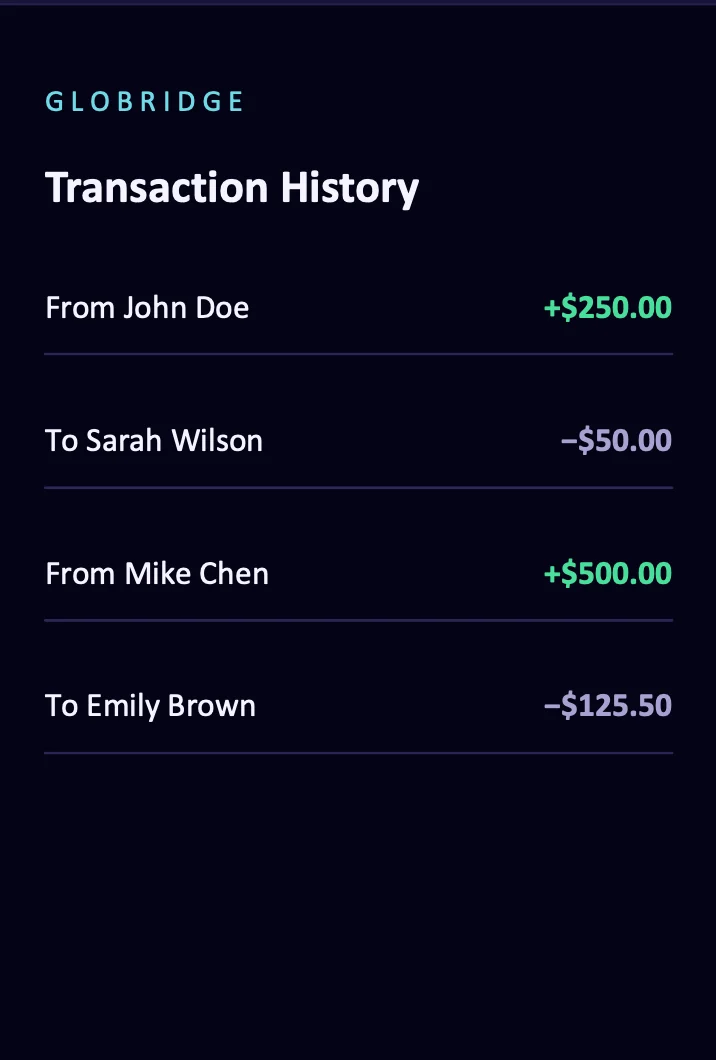

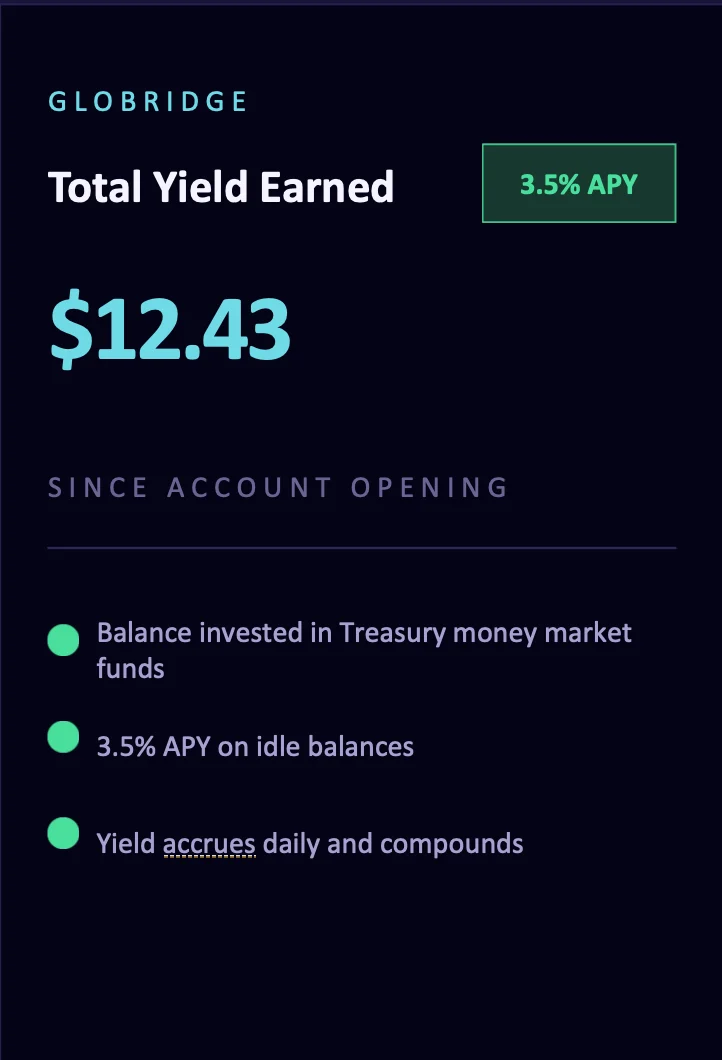

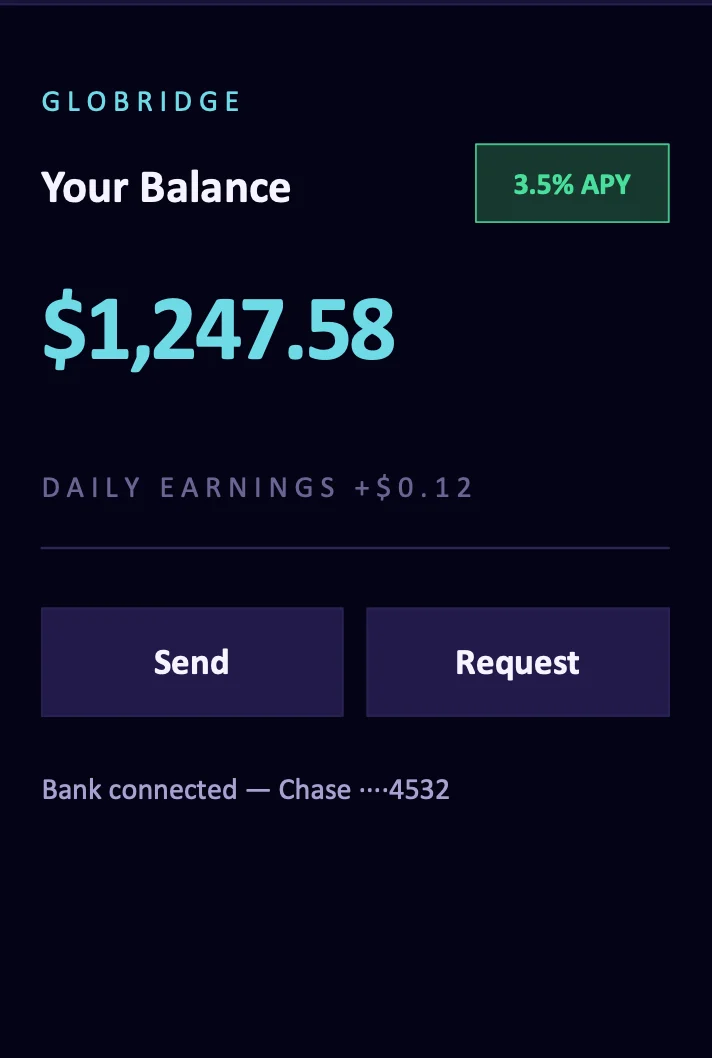

Designed around clarity after every transfer.

Globridge product concepts emphasize clear transaction history, recipient-level visibility, and status-aware account activity. The public launch experience may differ as the beta is refined through user testing, partner review, and compliance requirements.

Product is in development. Screens are illustrative concepts. Final names, amounts, percentages, features, disclosures, and availability may change before public launch. Yield-related concepts are experimental and not final; any balance-related benefits would be subject to eligibility, legal and regulatory approval, partner terms, and customer disclosures.

Modern rails. Familiar experience.

Global payments are being rebuilt around faster, more programmable dollar infrastructure. Globridge keeps the customer experience familiar while using approved backend infrastructure only where it can improve settlement, liquidity movement, transparency, or cost.

Stablecoin infrastructure has reached institutional scale, but raw blockchain activity can include trading, treasury movement, and other non-consumer activity. That is why Globridge treats stablecoins as backend rails, not as the product identity. Customers should not need to manage crypto wallets, private keys, blockchain networks, gas fees, token tickers, or self-custody workflows.

Behind the scenes, Globridge evaluates supported routes.

Globridge is designed to coordinate payment, payout, compliance, and settlement workflows behind the scenes. Users see a simple transfer experience, while supported routes are evaluated based on availability, cost, timing, compliance requirements, and operational reliability.

Sources: Bloomberg reported 2025 stablecoin transaction volume of approximately $33T, up 72%, citing Artemis Analytics; Visa reports adjusted stablecoin volume and circulating supply on its stablecoin analytics materials. Bloomberg · Visa

Start focused. Expand carefully.

The roadmap separates what Globridge is preparing for launch from future account and payment features that depend on partner support, legal review, regulatory requirements, eligibility, disclosures, and operational readiness.

Launch focus

U.S.–Philippines transfers, clear quotes, transfer tracking, supported payout options, and support workflows.

Account roadmap

USD-linked value tools, potential balance-related benefits, and recipient-side account utility, if supported by applicable law, partner structure, disclosures, and eligibility.

Future payment use cases

Merchant and service-provider payments, additional corridors, and broader cross-border workflows after launch validation.

Security, compliance, and operating discipline.

Globridge is being built for a regulated financial-services environment, with emphasis on partner oversight, risk controls, reconciliation, and customer clarity.

Some reviews protect users and support compliance.

Globridge is being designed with controls for identity verification, account access, unusual transfer behavior, payout changes, sanctions screening, and transaction-risk monitoring. Some transfers may be delayed, reviewed, limited, or declined to protect users and meet compliance requirements.

Onboarding is expected to include identity, eligibility, and risk review through approved infrastructure providers.

Transfers are designed to support risk checks, status tracking, exception workflows, and escalation procedures.

The operating model prioritizes ledger records, payout status, partner reporting, exception handling, and daily reconciliation.

Product development includes attention to secure systems, access controls, auditability, and responsible handling of customer data.

Partner-led regulated infrastructure

Globridge does not currently hold state money transmitter licenses. The intended launch model is to work with regulated banking, payments, and infrastructure partners that support applicable licensed or regulated components of the transaction flow.

Globridge remains responsible for its own product design, customer experience, operational controls, partner oversight, disclosures, support, data security, and compliance program development. Availability will depend on partner approval, legal review, and supported jurisdictions.

To report a security concern, contact security@globridgepay.com.

Availability.

Globridge is preparing for a controlled launch, beginning with one focused corridor before expanding availability.

United States → Philippines

Globridge is starting with a focused corridor so we can validate pricing clarity, payout reliability, support workflows, compliance controls, and user experience before expanding.

Additional corridors to be announced

Future corridors, features, limits, and payout methods will depend on user demand, partner approval, legal and regulatory review, supported jurisdictions, and operating readiness.

Built by a cross-functional founding team.

The Globridge team combines payments strategy, finance, engineering, economics, policy, operations, and go-to-market experience. Globridge has been selected for Phase II of the University of Chicago Polsky Center’s New Venture Challenge.

Nicholas Yun

Leads strategy, financing, partner development, unit economics, and corridor positioning. Background in venture analysis, financial modeling, market research, and investor materials.

Mingyu Du

Leads operations and product execution. Background in quantitative finance, credit-risk modeling, financial analysis, venture building, and customer-experience development.

Haowen Xia

Leads engineering and infrastructure. Experience across backend systems, cloud and DevOps, AI applications, FastAPI, SpringBoot, and production-oriented technical workflows.

Yu Shi

Leads corridor economics, policy analysis, quantitative risk modeling, and stablecoin-related research. Background in econometrics, microeconomic theory, finance, and statistical modeling.

Virginia R. Washington

Leads go-to-market, customer acquisition, and partnerships. Background in venture investing, policy research, institutional strategy, startup acceleration, and international development.

Team biographies are summarized for a consumer audience and avoid personal contact details.

Advisory network.

Globridge is informed by advisors with experience across global remittance, emerging-market payments, fintech infrastructure, capital formation, and strategic finance. Their perspectives help the team evaluate product design, operating discipline, partner readiness, and long-term scalability.

Alex Holmes

Alex brings senior operating perspective from global money movement, including leadership experience at MoneyGram and Western Union. His background informs Globridge’s thinking on corridor strategy, payout reliability, compliance-aware operations, and the practical requirements of scaling a trusted remittance product.

Mateo Bermeo Motta

Mateo contributes operating perspective across Latin American payments, fiat-to-digital-asset infrastructure, and emerging-market financial access. His experience helps Globridge evaluate partner-led payment workflows, market-specific user needs, and the operational realities of serving cross-border customers.

Joseph Ender

Joseph provides a financial-infrastructure and investor-diligence perspective shaped by fintech M&A, capital markets, and private-equity investing. His input supports Globridge’s approach to business model discipline, strategic positioning, financing readiness, and long-term enterprise value creation.

Advisors provide strategic perspective and do not provide consumer financial services, banking services, custody, money transmission, legal advice, investment advice, or guarantees on behalf of Globridge.

Execution bench.

Globridge is also supported by a broader execution bench across software engineering, data systems, product strategy, infrastructure, and quantitative risk modeling.

Monica Wang

Software engineering and data systems support, with experience across Amazon and data science work with the United Nations.

William Wang

Supports strategy, research, and product development, with experience across Chicago Booth, BCG, OCBridge, Cornell, and UIUC.

Gavin Guan

Supports systems infrastructure, automation, verification, and technical tooling, with engineering experience at AMD.

Joe Tam

Supports quantitative risk modeling and financial risk analysis, with a Yale Finance PhD background and quantitative finance expertise.

Execution bench contributors support Globridge’s development and operating readiness; roles and involvement may evolve as the company progresses toward launch.

Join the Globridge launch waitlist.

Be notified when Globridge becomes available in your corridor. We are beginning with a controlled U.S.–Philippines launch and will expand availability over time.

Email is required. All other fields are optional and help us understand corridor demand. Joining the waitlist does not create an account, initiate onboarding, transmit money, hold funds, or provide access to financial services.

FAQ

Answers to common questions about availability, product scope, compliance posture, and planned features.

Is Globridge available to the public?

Globridge is currently in development. The launch waitlist is for users who want to be notified as availability expands. The beta environment is separate and should be accessed only through the “Open beta app” button in the navigation.

Is Globridge a crypto trading app?

No. Globridge is not designed as a crypto trading or self-custody product. Users are not expected to manage private keys, select blockchain networks, pay gas fees, or trade digital assets. Any digital-asset infrastructure, where used, is intended to operate behind the scenes through approved partners.

Does Globridge hold money transmitter licenses?

Globridge does not currently hold state money transmitter licenses. Our intended launch model is to work with regulated banking, payments, and infrastructure partners that support the applicable licensed or regulated components of the transaction flow. Globridge is responsible for its own product design, customer experience, operational controls, partner oversight, disclosures, support, data security, and compliance program development. Availability will depend on partner approval, legal review, and supported jurisdictions.

Will users need to understand crypto or stablecoins?

No. Globridge is designed as a familiar cross-border money account. Backend settlement infrastructure may be used where appropriate, but users should not need to manage wallets, chains, private keys, gas fees, token tickers, or self-custody workflows.

What countries will Globridge support first?

The initial product focus is the U.S.–Philippines corridor. Additional corridors will depend on user demand, partner coverage, payout reliability, compliance review, and operational readiness.

Are USD-linked value tools, potential balance benefits, and merchant payments available today?

Not as public launch features unless and until they are approved, supported, and operationally ready. These are planned product directions that may become available only where legally permitted and supported by appropriate partner structures, disclosures, eligibility controls, and operating readiness.

How does the waitlist work?

Submit your email to receive launch updates. All other waitlist questions are optional and help Globridge understand corridor demand, transfer frequency, and product interest. Joining the waitlist does not create an account, initiate onboarding, transmit money, hold funds, or guarantee access. Indicating beta interest does not guarantee beta access.

Will Globridge support languages other than English?

The initial consumer experience is expected to launch in English. Filipino-language support, including Tagalog and potentially additional regional language support, may be evaluated as the U.S.–Philippines launch develops.

Globridge is not a bank. Product features, transfer availability, pricing, timing, balance features, and payout options are subject to partner support, eligibility, legal review, and applicable regulatory requirements.